Global air passenger demand rose 2.1% year on year in March, but the headline figure masked a near-total collapse in Middle Eastern traffic caused by the US-Israel-Iran war, the International Air Transport Association (IATA) said in data released on April 29.

Traffic at Middle Eastern carriers fell 60.8% compared with March 2025, with capacity down 56.9% and load factors slipping 6.6 percentage points to 67.8%, IATA said. The decline reflected the closure of much of the region’s airspace following the conflict that began on February 28.

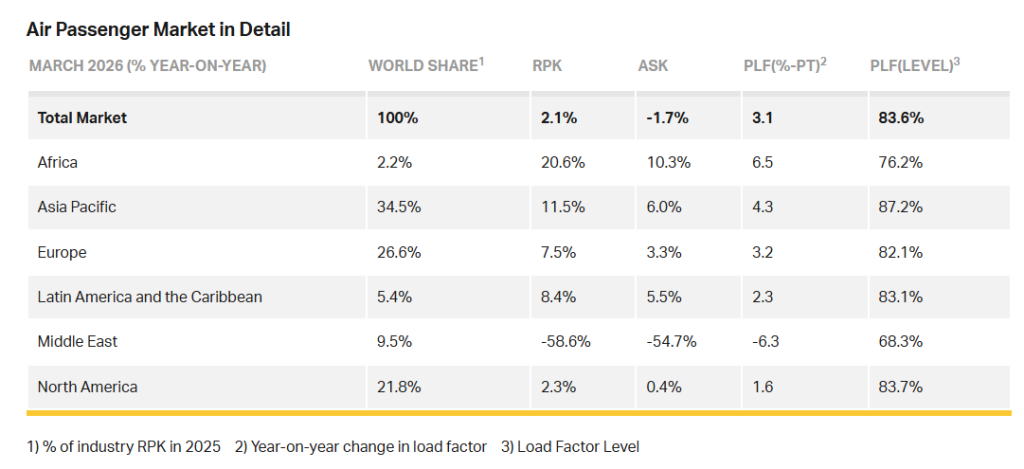

Stripping out the Middle East, international demand grew by around 8% globally. Total international revenue passenger kilometres (RPK) fell 0.6% year on year, the first international contraction since March 2021. Worldwide capacity dropped 1.7%, while the load factor climbed 3.1 percentage points to 83.6% as carriers filled more seats on a smaller schedule.

“Demand for air travel continued to grow in March despite disruptions in the Middle East,” IATA director general Willie Walsh said in a statement. “The nearly 61% decline in international traffic by carriers in the Middle East did, however, restrain global growth to 2.1%.”

Walsh flagged jet fuel as the principal risk to the northern hemisphere summer season. Asia and Europe, both heavily dependent on Gulf supplies, could face shortages over the coming months, while elevated fuel prices were already feeding through to ticket prices, he said. Forward bookings have so far held up, with the summer “shaping up to be a normally busy time for travel”.

The disruption has redrawn intercontinental traffic flows. European carriers posted a 7.7% rise in demand, with Europe-Asia traffic surging 29.3% as direct services replaced routings that previously transited Gulf hubs. Asia-Pacific airlines recorded an 11.5% increase in demand and a regional load factor of 91.2%, the highest of any region. North American carriers grew 3.7%, with transatlantic traffic up 3.3%.

African carriers led the percentage growth tables, with demand rising 19.2% year on year, while Latin American airlines posted a 12.1% increase.

Domestic markets continued to expand, with global domestic RPK up 6.5% and capacity up 5.6%. China and Brazil posted double-digit growth, with Australia and Japan also accelerating. Indian domestic traffic fell, which IATA attributed to reduced feeder flights into hubs serving the Middle East.

Walsh urged regulators to grant carriers flexibility on airport slot rules given the airspace constraints and the prospect of fuel rationing. “Airline resilience is being tested and stabilising the supply and price of fuel is crucial,” he said.

The figures land as carriers including flydubai, Air Arabia, Oman Air and Royal Jordanian have begun returning to Doha’s Hamad International Airport under a phased reopening agreed with the Qatar Civil Aviation Authority. Gulf Air, Ethiopian Airlines and Indian carriers are due to follow in May.