GCC hotel owners and investors have turned cautious but not bearish on the region’s hospitality sector following the 2026 US-Iran conflict, with capital preservation now dominating short-term strategy even as long-term confidence holds, according to a survey by hospitality consultancy HVS published on May 19.

The survey of hotel owners, developers, investors and hospitality-focused real estate groups representing an estimated 160,000 branded hotel rooms across the GCC found that the disruption is being transmitted primarily through aviation connectivity and traveller confidence rather than a structural collapse in demand. Saudi Arabia accounted for 42% of respondents and the United Arab Emirates 34%, with the balance spread across Kuwait, Bahrain, Oman and Qatar.

The wider region was losing roughly $600mn a day in visitor spending during the peak period of disruption, according to estimates from the World Travel and Tourism Council cited in the report. The timing amplified the financial hit, with the conflict escalating between March and May, one of the GCC’s highest-yield trading periods, dominated by religious travel, spring leisure demand, MICE activity and international tourism.

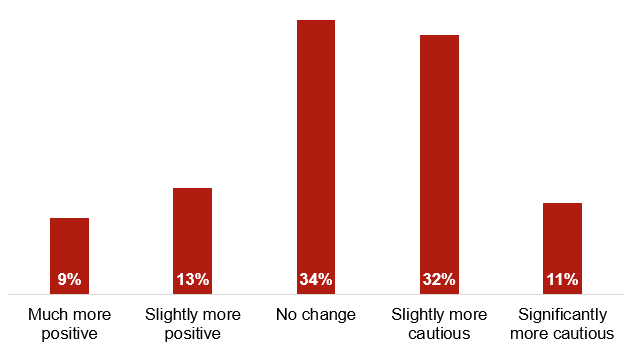

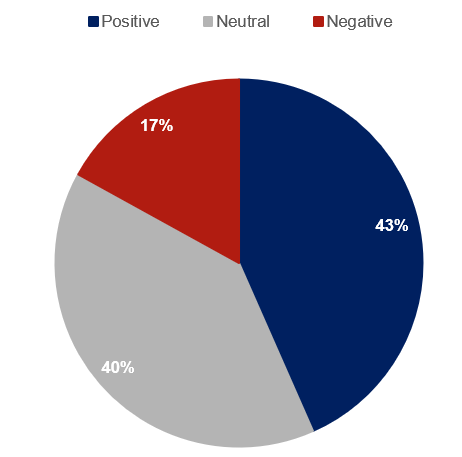

Sentiment has shifted markedly. Around 43% of respondents have become more cautious since the conflict, including 11% significantly so, although 22% report a more positive outlook and 34% see no change. A combined 83% described their investment outlook as positive or neutral, a result the report called notable given the scale of the geopolitical shock.

Investment Sentiment: Confidence Weakens but Does Not Collapse

The performance gap between asset types has widened. Hotels supported by domestic demand, religious travel and staycation activity have proved more resilient, while assets dependent on international arrivals, airline connectivity and corporate and MICE demand remain more exposed. A combined 76% of respondents reported moderate or significant negative impact on revenue per available room, with nearly half seeing declines of more than 20%.

Capital preservation has become the dominant near-term strategy. Investors are preserving cash, deferring capital expenditure, slowing development and renegotiating operator terms. Around 45% of respondents reported delays to investment or development decisions, including 18% citing significant delays. Most expect EBITDA recovery within 6 to 12 months, although the report cautioned that occupancy recovery alone would not necessarily restore profitability given pressure on average daily rates, operating cost inflation and supply chain costs.

Hospitality Investment Outlook Remains Structurally Positive

The market is not frozen. A combined 41% of respondents still intend to build or acquire hospitality assets, while sell intentions remain very limited. Around 57% said their assets could meet key financial obligations for at least six months if current conditions persisted.

Respondents identified disruption to regional air connectivity as the single greatest risk facing GCC hospitality investment, with weaker leisure demand, softer corporate and MICE activity, the risk of wider regional escalation and rising construction and operating costs also flagged.

The report concluded that the GCC hospitality sector is entering a period defined less by retreat than by disciplined capital deployment, selective expansion and a greater focus on operational resilience, with long-term tourism growth, religious travel, national tourism strategies and infrastructure expansion continuing to underpin investor interest.

Selectivity Becomes the Defining Investment Theme

Why it matters for the trade

For operators, agents and asset managers, the survey signals a market that is recalibrating rather than retreating. Capital is still being deployed, but on tighter criteria. Properties weighted to domestic and religious travel are likely to keep advancing on schedule, while internationally-exposed and MICE-dependent assets face slower recovery, longer underwriting timelines and harder financing conversations. The aviation recovery sets the ceiling for everything else: until connectivity and traveller confidence return, hotel performance will lag.

Link to original report.