Saudi Arabia’s hotel market split in two during the first quarter of 2026. Domestic travellers and religious pilgrims propped up occupancy and rates. International and business demand pulled back. The net result was a sector that looked broadly stable on paper while masking sharp differences between cities, according to new research from JLL.

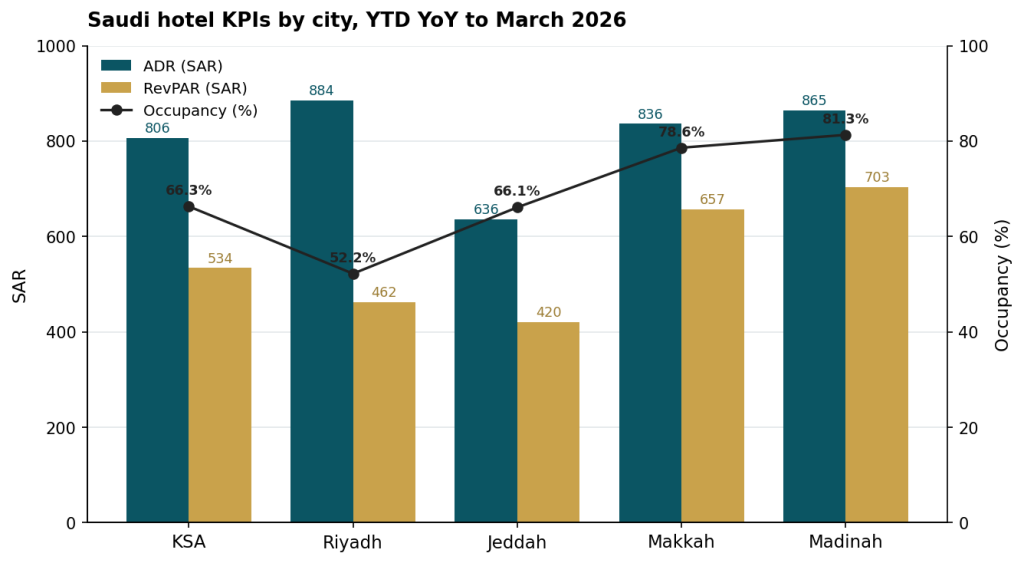

Nationwide occupancy reached 66.3% in the year to March 2026. Average daily rate rose 3.0% to SAR805.5. Revenue per available room came in at SAR533.7, down 1.3%. The headline decline was modest. The story underneath was not.

Ramadan and Eid did the heavy lifting. Both fell within the quarter and drove religious visits to Makkah and Madinah alongside family travel across the Kingdom. International arrivals fell year-on-year. Total visitation, counting inbound and domestic together, held comparatively flat.

Domestic travel anchors a softer quarter

The Kingdom recorded 28.9 million domestic tourists in the quarter. That base did most of the work. JLL frames domestic demand as a stabilising mechanism, a buffer against weaker inbound numbers tied to regional geopolitical conditions.

A large share of the activity came from pilgrimage. Religious visits to Makkah and Madinah during Ramadan sustained baseline demand in the holy cities. Beyond faith-based travel, the Eid holiday produced strong leisure demand at The Red Sea, the flagship of Saudi Arabia’s push to widen its tourism offer past pilgrimage. JLL reads that uptick as evidence the diversification strategy is starting to land with domestic travellers.

The divergence is structural. Religious destinations carry consistent pilgrimage traffic. Commercial hubs and gateway cities stay exposed to swings in international and business travel. The first quarter exposed that gap rather than created it.

City performance: Riyadh down, Jeddah up, holy cities steady

Riyadh had the weakest quarter of the major markets. Occupancy fell 13.5 percentage points to 52.2%. RevPAR dropped 9.5% to SAR461.8. ADR still climbed 4.6% to SAR884.3, the highest rate of any tracked city, but rate growth could not offset the volume loss. The capital’s reliance on corporate and international demand left it most exposed.

Jeddah moved the other way. Occupancy gained 3.8 percentage points to 66.1%. ADR edged up 0.5% to SAR635.7. RevPAR rose 4.4% to SAR420.4. The gateway city posted the strongest RevPAR growth of the group.

The holy cities held firm through Ramadan. Makkah ran at 78.6% occupancy with ADR at SAR836.0, lifting RevPAR 0.5% to SAR657.2. Madinah posted the highest occupancy in the Kingdom at 81.3%, with ADR up 3.6% to SAR864.8 and RevPAR up 2.0% to SAR703.3. Madinah also recorded the strongest ADR growth nationally.

| Market | ADR (SAR) | Occupancy | RevPAR (SAR) | ADR change | Occupancy change | RevPAR change |

|---|---|---|---|---|---|---|

| KSA | 805.5 | 66.3% | 533.7 | +3.0% | -4.2pp | -1.3% |

| Riyadh | 884.3 | 52.2% | 461.8 | +4.6% | -13.5pp | -9.5% |

| Jeddah | 635.7 | 66.1% | 420.4 | +0.5% | +3.8pp | +4.4% |

| Makkah | 836.0 | 78.6% | 657.2 | +0.1% | +0.4pp | +0.5% |

| Madinah | 864.8 | 81.3% | 703.3 | +3.6% | -1.5pp | +2.0% |

Supply growth stays measured

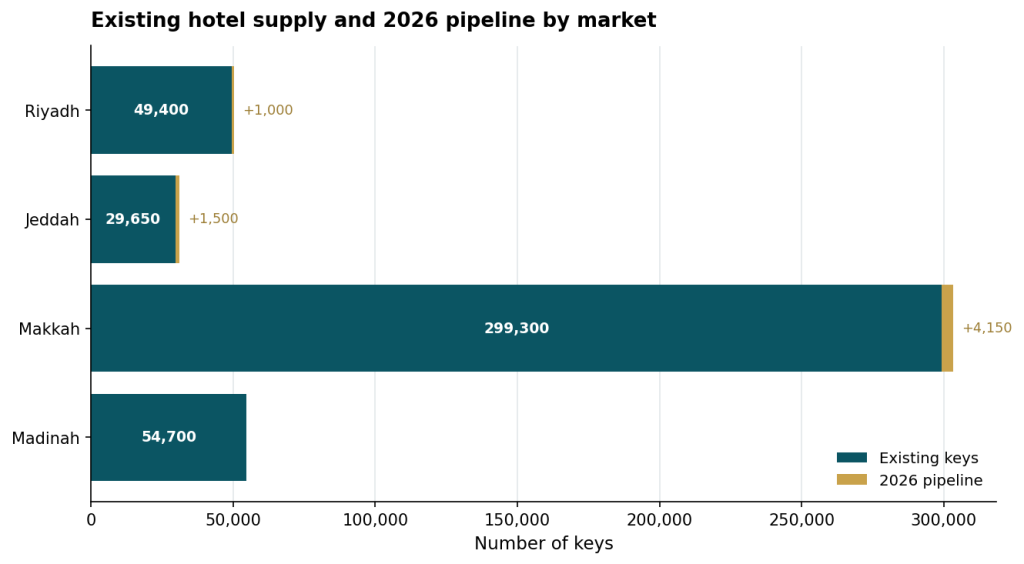

Developers held back. Riyadh added roughly 110 keys in the quarter to reach around 49,400 keys. Jeddah recorded no completions and stayed at about 29,650 keys. The rest of 2026 is set to bring around 1,000 more keys in Riyadh and 1,500 in Jeddah, keeping competitive pressure on operators as new inventory comes online.

Makkah added about 1,700 keys to reach around 299,300, with a further 4,150 keys expected through the year. That weight of supply makes segmentation, pricing and asset differentiation central to capturing visitor flows. Madinah recorded no completions and held at roughly 54,700 keys.

JLL describes first-quarter delivery as measured, with developers adopting phased strategies tied to demand. The approach supports near-term stability and keeps new inventory closer to absorption capacity.

Outlook: sensitive in the near term, structurally intact

The sector is working through moderated demand after a soft quarter. Regional geopolitical tension constrained inbound tourism. Ramadan held the floor, especially in religious destinations, but international visitor sentiment stayed cautious and demand spread unevenly across cities.

That composition is the key variable. Religious tourism gives the holy cities a stable base. Commercial hubs and leisure destinations remain open to outside shocks. Domestic and regional travel are the stabilisers, and operators are leaning on targeted offers, seasonal packaging and pricing adjustments to cover thinner international inflows.

Guest behaviour is shifting too. Shorter stays, value-led bookings and experiential travel are reshaping how operators run their assets. The response runs to flexible pricing, more amenities and tighter integration into mixed-use and lifestyle developments.

The fundamentals sit on government tourism programmes, infrastructure spending and expansion plans. Near-term performance stays sensitive to external factors. The structural base holds. Recovery tracks the return of inbound travel and a calmer regional picture.

Performance data sourced from STR Global. Tourism, supply and pipeline data from JLL Research, Q1 2026. ADR and RevPAR figures in Saudi riyal (SAR).